Case Study

Case Study

Pool | Collaborative & Personal Savings

Collaborative savings platform enabling structured group financial goals and transparent contribution tracking.

Collaborative savings platform enabling structured group financial goals and transparent contribution tracking.

Problem Context

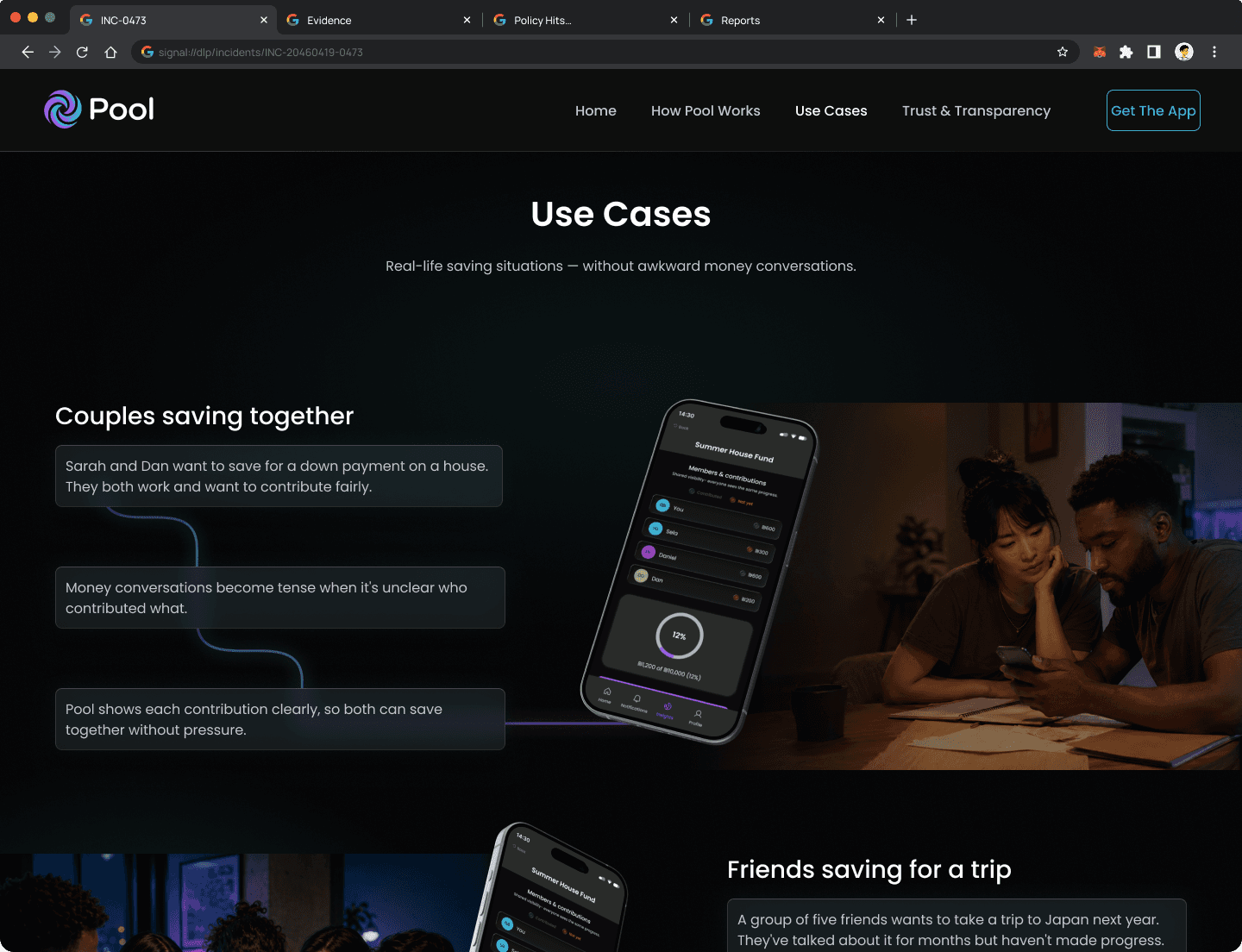

Saving toward a shared goal breaks down fast. Without one place to track who contributed what, groups fall back on messages and mental math. Pool gives everyone a shared view that updates automatically, no check-ins needed.

No clear view of who contributed what.

No clear view of who contributed what.

No clear view of who contributed what.

Progress feels abstract and unmotivating.

Progress feels abstract and unmotivating.

Progress feels abstract and unmotivating.

Asking about money creates tension.

Asking about money creates tension.

Asking about money creates tension.

Designed in dialogue with Figma Make

Designed in dialogue with Figma Make

Key screens and component variants were explored using Figma Make as an active design partner. Generating layout alternatives, testing edge cases, and stress-testing the contribution flow before committing to final decisions.

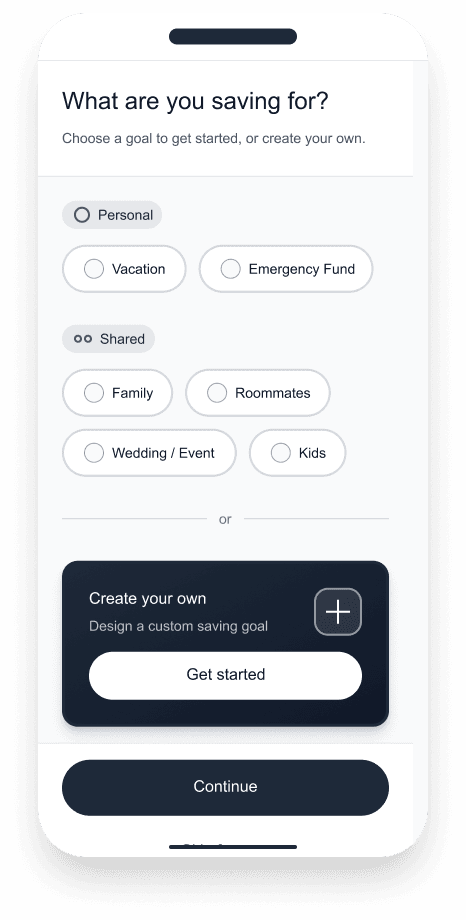

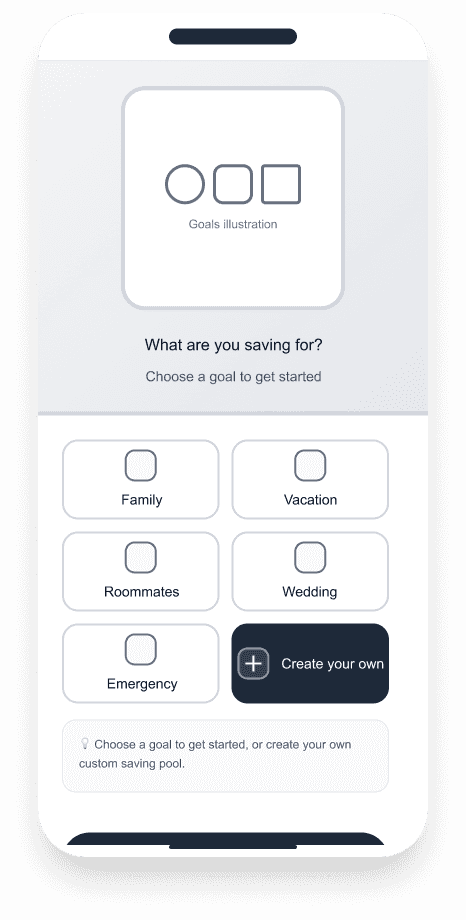

Saving goals screen options

Option 1- Grid

Option 2- Carousel

Option 3- List

Option 4- Segments

Option 5- Split

Option 1- Grid

Option 2- Carousel

Option 3- List

Option 4- Segments

Option 5- Split

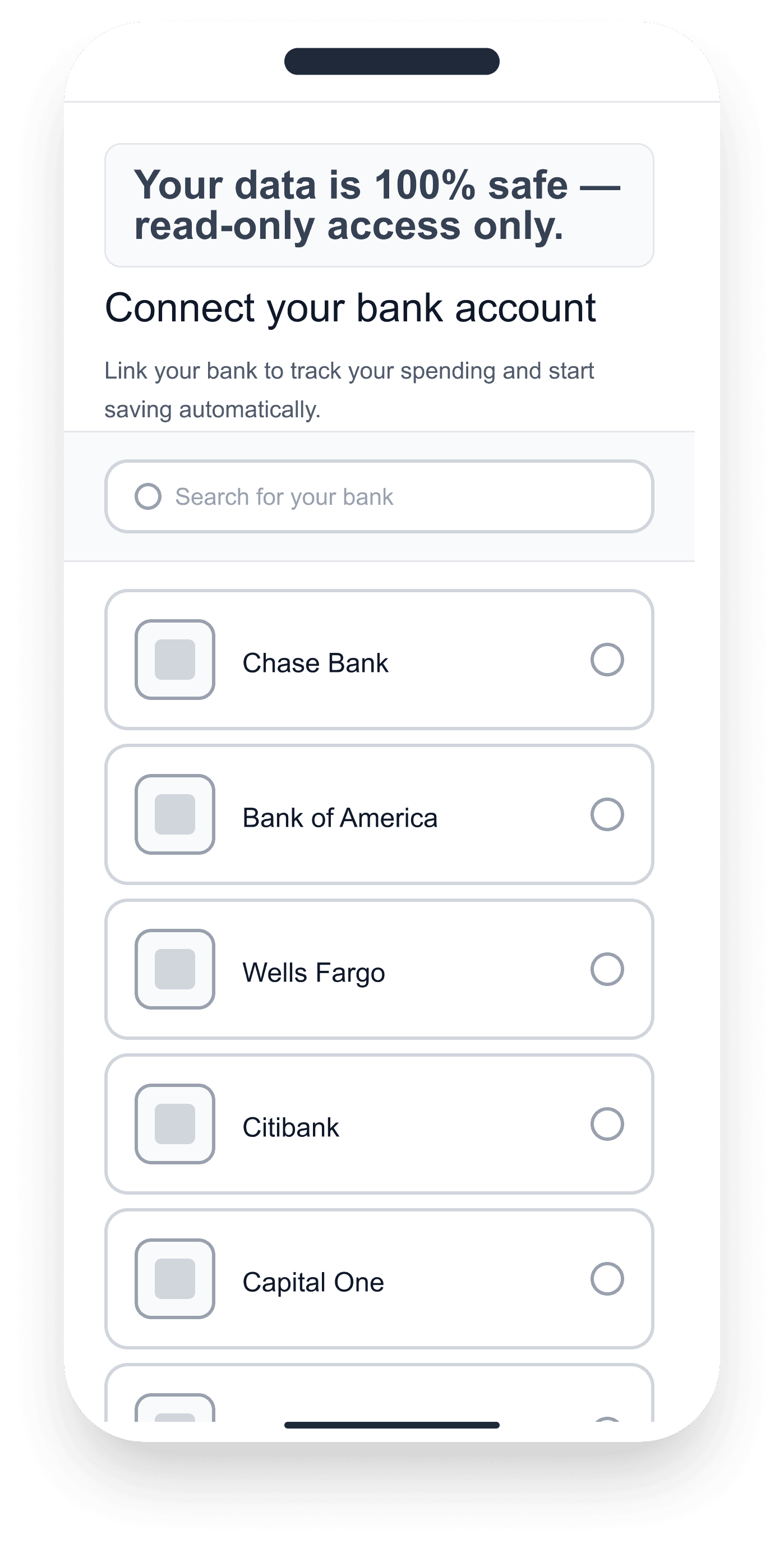

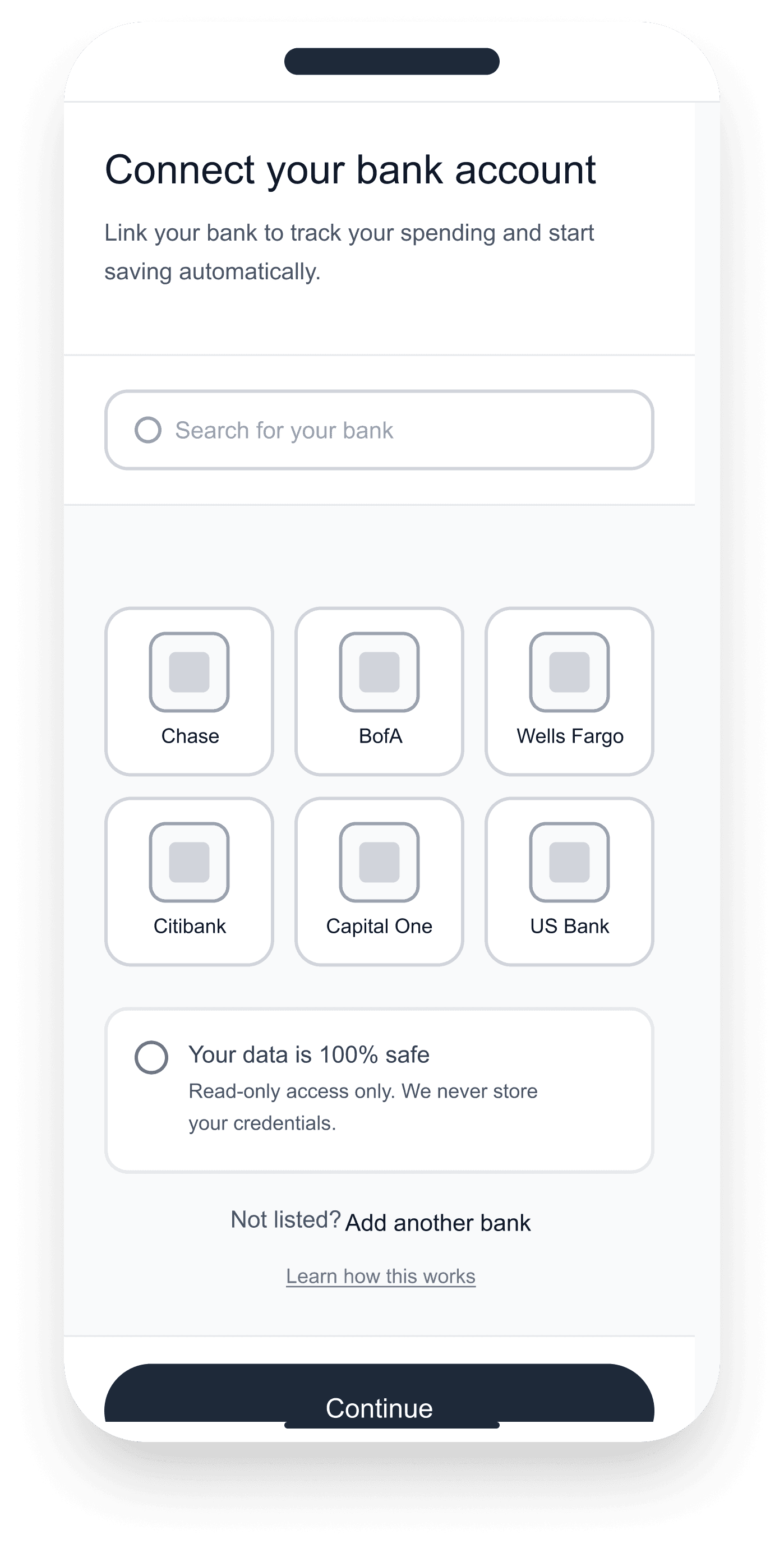

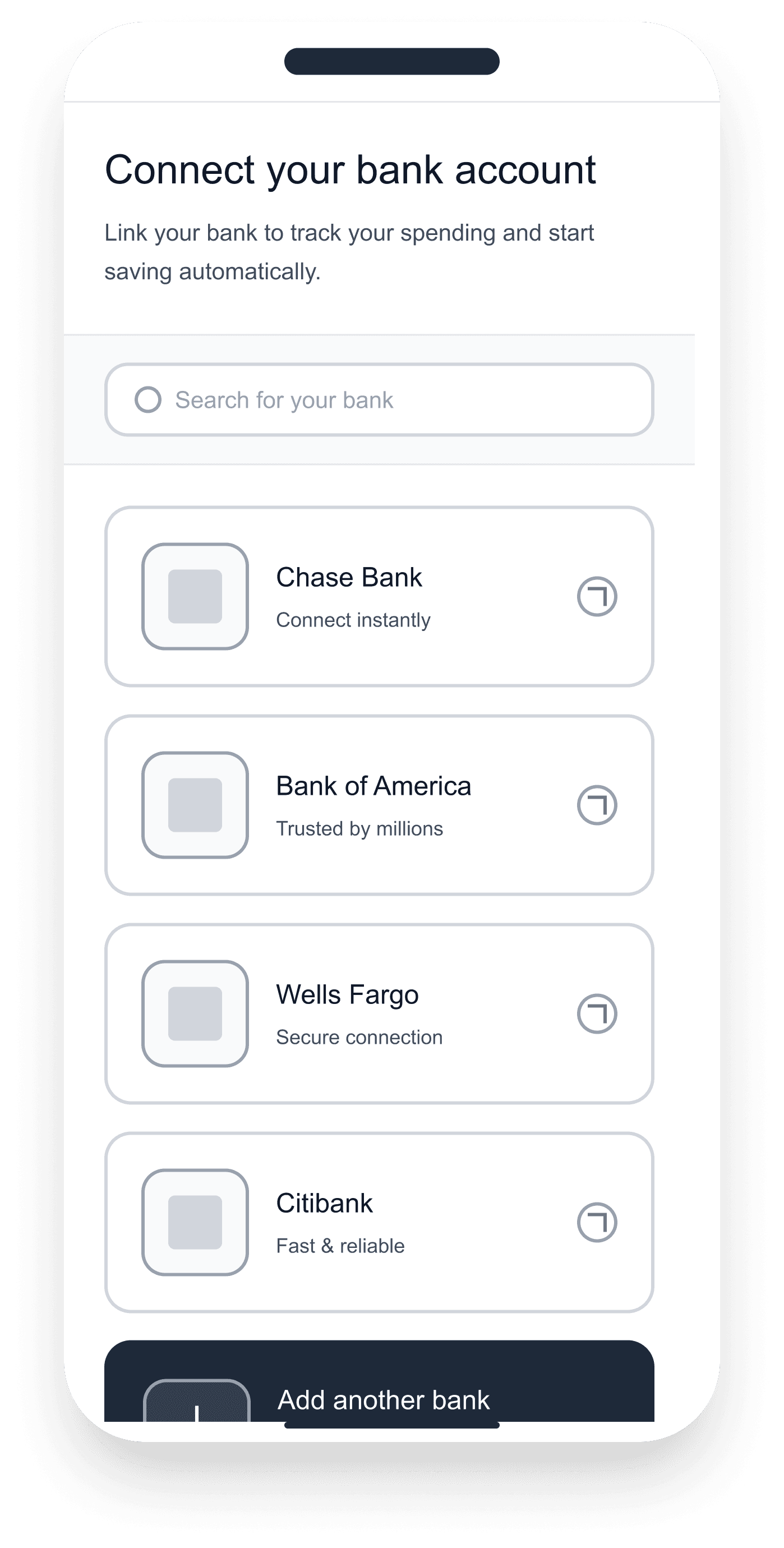

Connect Bank screen options

Option 1- List

Option 1- List

Option 2- Grid

Option 2- Grid

Option 3- Cards

Option 3- Cards

Option 4- Modal

Option 5- Split

Option 5- Split

Option 1- List

Option 2- Grid

Option 3- Cards

Option 4- Modal

Option 5- Split

Design Decisions & Trade-off

Design Decisions & Trade-off

Three decisions shaped Pool. Each one had a cost, and each cost was chosen deliberately.

Spectrum, not binary

The same Pool structure serves personal goals and shared goals. People track progress the same way alone or together, so two interfaces would mean learning the same task twice. The trade-off: shared-only features like invitations and member visibility had to feel optional in personal mode, not like a second product.

Spectrum, not binary

The same Pool structure serves personal goals and shared goals. People track progress the same way alone or together, so two interfaces would mean learning the same task twice. The trade-off: shared-only features like invitations and member visibility had to feel optional in personal mode, not like a second product.

Spectrum, not binary

The same Pool structure serves personal goals and shared goals. People track progress the same way alone or together, so two interfaces would mean learning the same task twice. The trade-off: shared-only features like invitations and member visibility had to feel optional in personal mode, not like a second product.

Transparency Vs. Comparison Anxiety

Showing each member's amount removes awkward questions, but it also invites comparison. "Dan saved 32%, I saved 17%." Pool shows progress, not performance. No leaderboards, no penalties, no nudging. The trade-off: full transparency demands careful copy and visual treatment to stay supportive rather than judgmental.

Transparency Vs. Comparison Anxiety

Showing each member's amount removes awkward questions, but it also invites comparison. "Dan saved 32%, I saved 17%." Pool shows progress, not performance. No leaderboards, no penalties, no nudging. The trade-off: full transparency demands careful copy and visual treatment to stay supportive rather than judgmental.

Transparency Vs. Comparison Anxiety

Showing each member's amount removes awkward questions, but it also invites comparison. "Dan saved 32%, I saved 17%." Pool shows progress, not performance. No leaderboards, no penalties, no nudging. The trade-off: full transparency demands careful copy and visual treatment to stay supportive rather than judgmental.

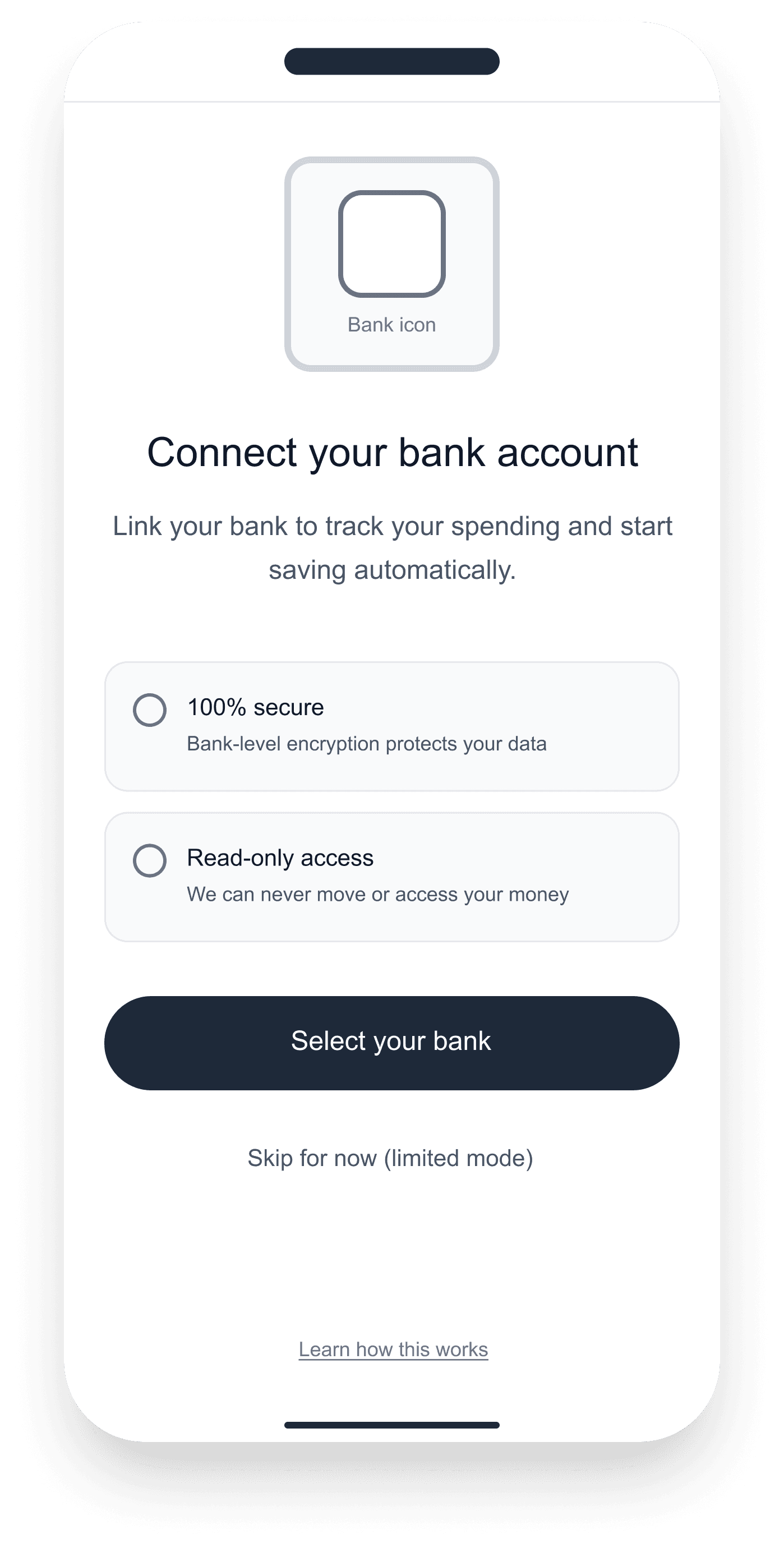

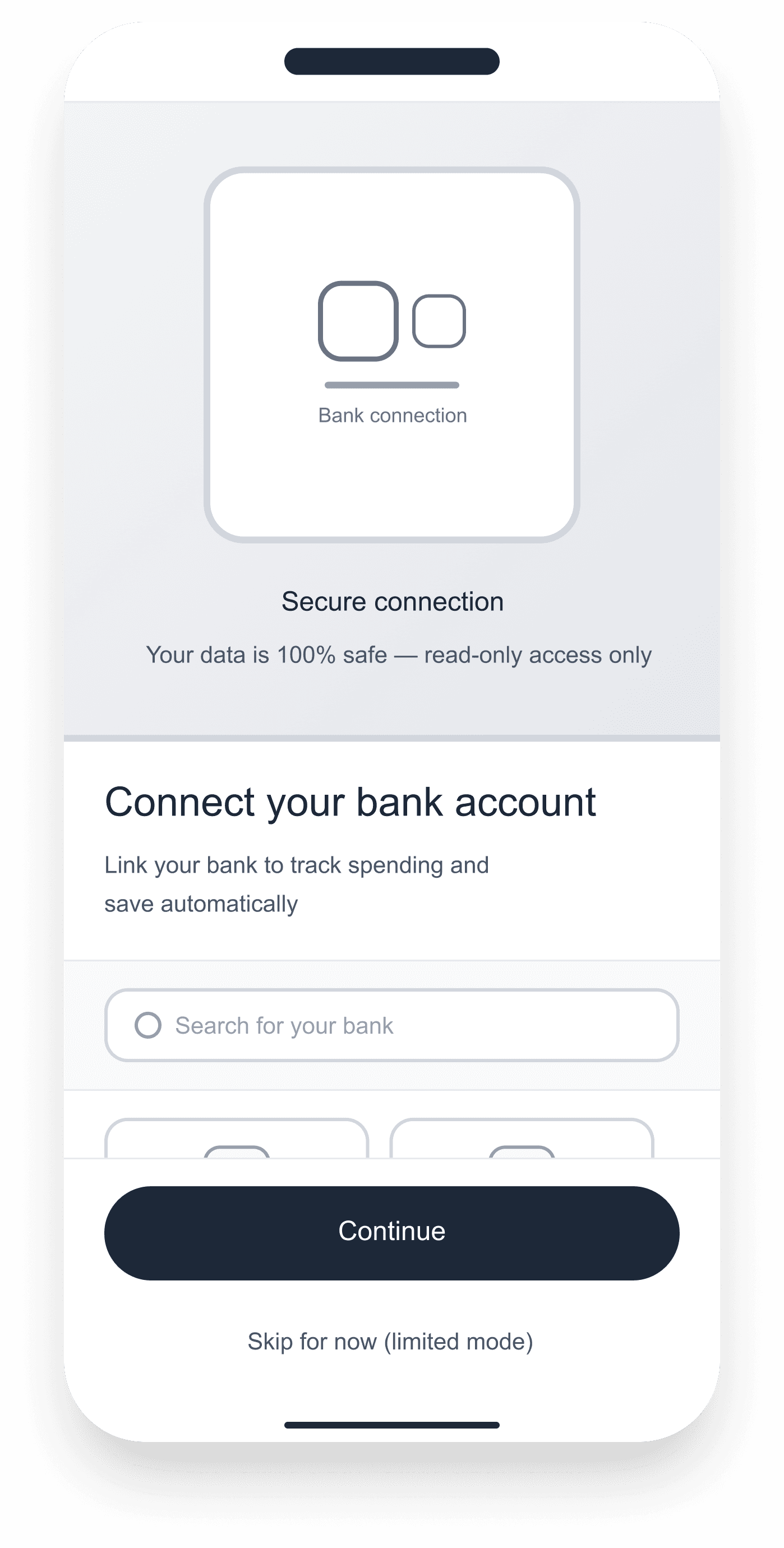

Bank Connection Vs. Onboarding Friction

Bank sync makes contributions accurate and automatic, but asking for credentials is the highest-friction step in onboarding. Pool offers bank connection as the primary path and "continue without bank" as a legitimate choice, not a fallback. The trade-off: less accurate data for manual users, but no cliff that loses people before their first pool.

Bank Connection Vs. Onboarding Friction

Bank sync makes contributions accurate and automatic, but asking for credentials is the highest-friction step in onboarding. Pool offers bank connection as the primary path and "continue without bank" as a legitimate choice, not a fallback. The trade-off: less accurate data for manual users, but no cliff that loses people before their first pool.

Bank Connection Vs. Onboarding Friction

Bank sync makes contributions accurate and automatic, but asking for credentials is the highest-friction step in onboarding. Pool offers bank connection as the primary path and "continue without bank" as a legitimate choice, not a fallback. The trade-off: less accurate data for manual users, but no cliff that loses people before their first pool.

One Mental Model

One Mental Model

Pool is built around one idea: define a target, track contributions, see where things stand. Whether saving alone or with a group, the structure is identical. One goal, one pool, one shared view of progress.

System Design

System Design

The system is built around a single contribution model, transparent, role-based, and immutable. Four layers govern how money moves, who sees what, and how the interface responds automatically.

1 - Contribution rules

Each pool defines its own input method and split logic, manual or bank-synced.

2 - Goal tracking

Progress is calculated automatically from validated transactions, no manual updates needed.

3 - Member roles

Visibility and permission rules are set at pool creation, no one can move money without an explicit action.

4 - Transparency layer

Every member sees a shared live view of progress and individual inputs, updated on every validated transaction.

1 - Contribution rules

Each pool defines its own input method and split logic, manual or bank-synced.

2 - Goal tracking

Progress is calculated automatically from validated transactions, no manual updates needed.

3 - Member roles

Visibility and permission rules are set at pool creation, no one can move money without an explicit action.

4 - Transparency layer

Every member sees a shared live view of progress and individual inputs, updated on every validated transaction.

The diagram below maps how these four layers translate into the token architecture. Foundation tokens define the grid and spacing rules. Surface and action tokens govern how contribution states appear. Status tokens trigger automatic responses when a payment is late or a goal is reached. Real-time goal tracking sits at the top, always visible, always current.

Token: surface/card

Token: surface/card

Token: surface/card

Scalable semantic architecture

Scalable semantic architecture

Scalable semantic architecture

Token: status/warning

Token: status/warning

Token: status/warning

Automated state response

Automated state response

Automated state response

Foundation: Radius-md

Foundation: Radius-md

Foundation: Radius-md

Modular system rule

Modular system rule

Modular system rule

Token: action/primary/bg

Token: action/primary/bg

Token: action/primary/bg

Predictable financial pattern

Predictable financial pattern

Predictable financial pattern

Token: surface/stack

Token: surface/stack

Token: surface/stack

Data-driven member display

Data-driven member display

Data-driven member display

Token: text/secondary

Token: text/secondary

Token: text/secondary

Real-time goal tracking

Real-time goal tracking

Real-time goal tracking

Token: text/primary

Token: text/primary

Token: text/primary

Predictable visual rhythm

Predictable visual rhythm

Predictable visual rhythm

Foundation: Spacing-md

Foundation: Spacing-md

Foundation: Spacing-md

Strict grid for visual trust

Strict grid for visual trust

Strict grid for visual trust

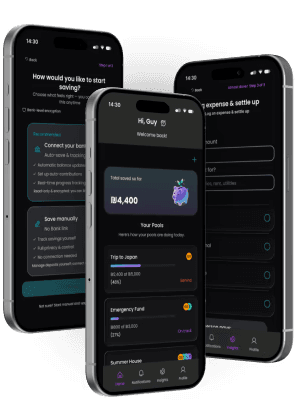

Key Screens

Core user flows demonstrating contribution clarity and shared visibility.

Core user flows demonstrating contribution clarity and shared visibility.

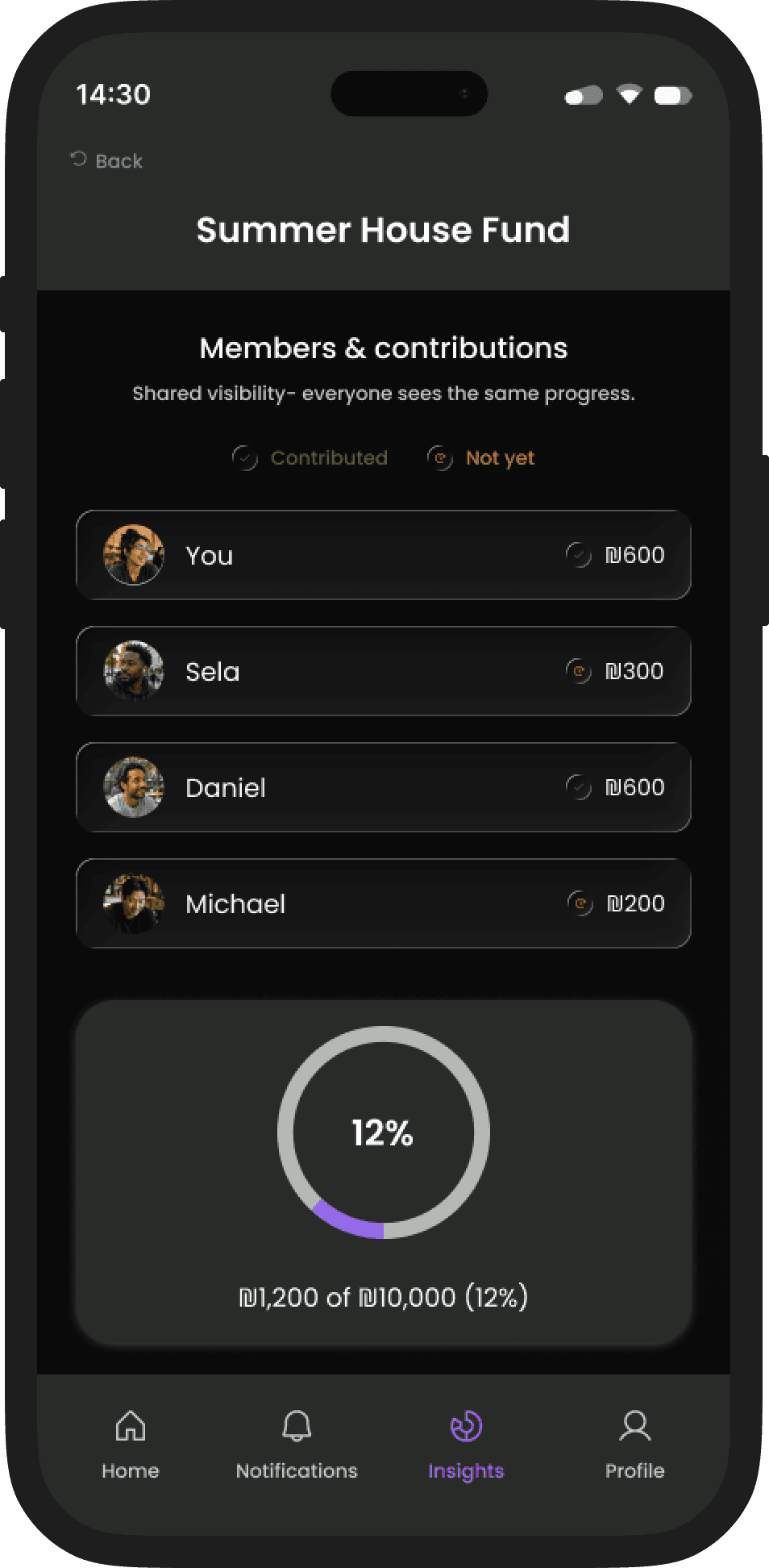

Shared Progress

Shared Progress

What this solves: group members can see who contributed and who hasn't, without anyone needing to ask.

What this solves: group members can see who contributed and who hasn't, without anyone needing to ask.

Transparency

Group accountability

Passive visibility

Contribution status is visible at a glance (Contributed / Not yet)

Contribution status is visible at a glance (Contributed / Not yet)

One shared view keeps accountability calm and consistent

One shared view keeps accountability calm and consistent

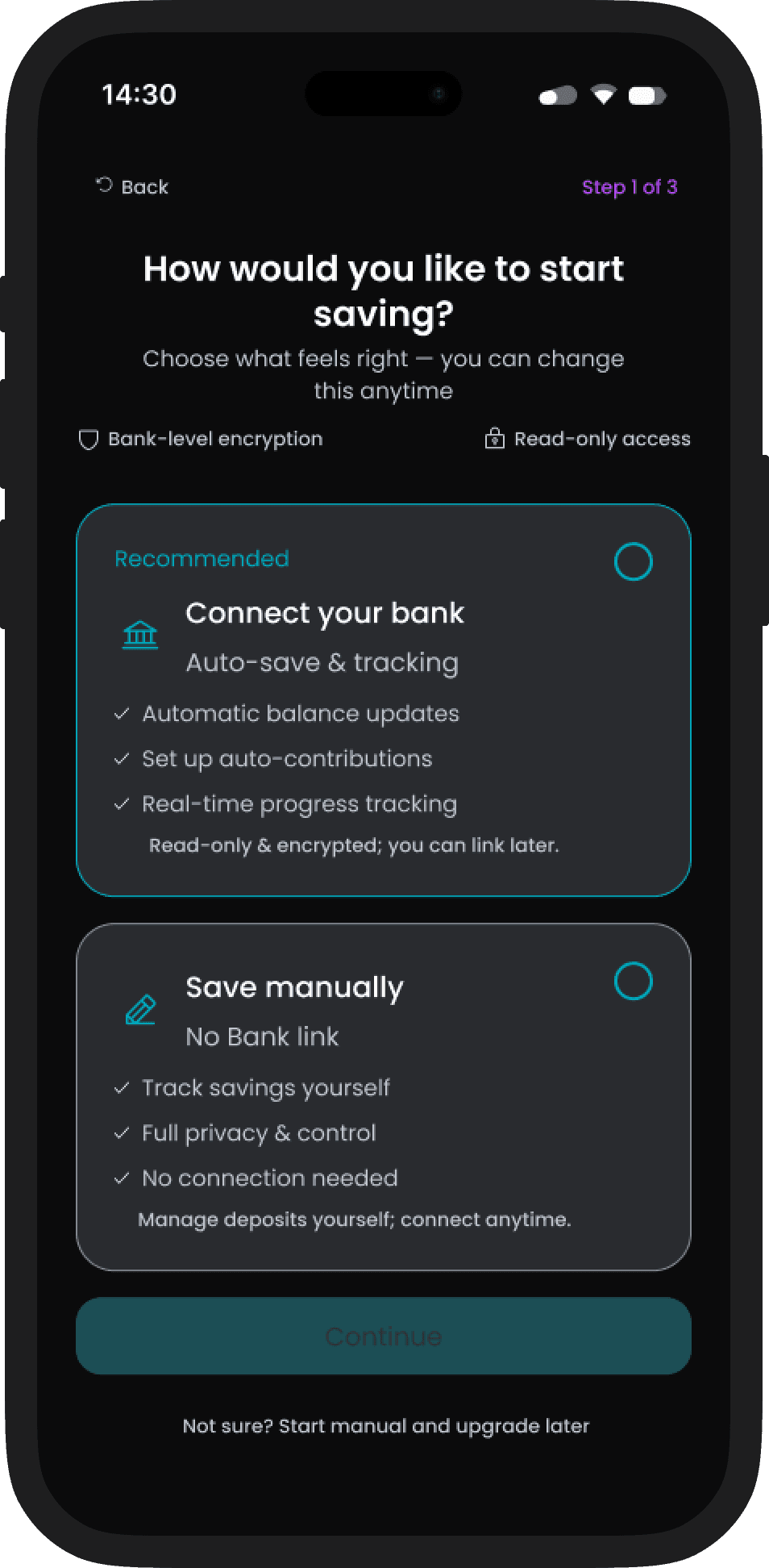

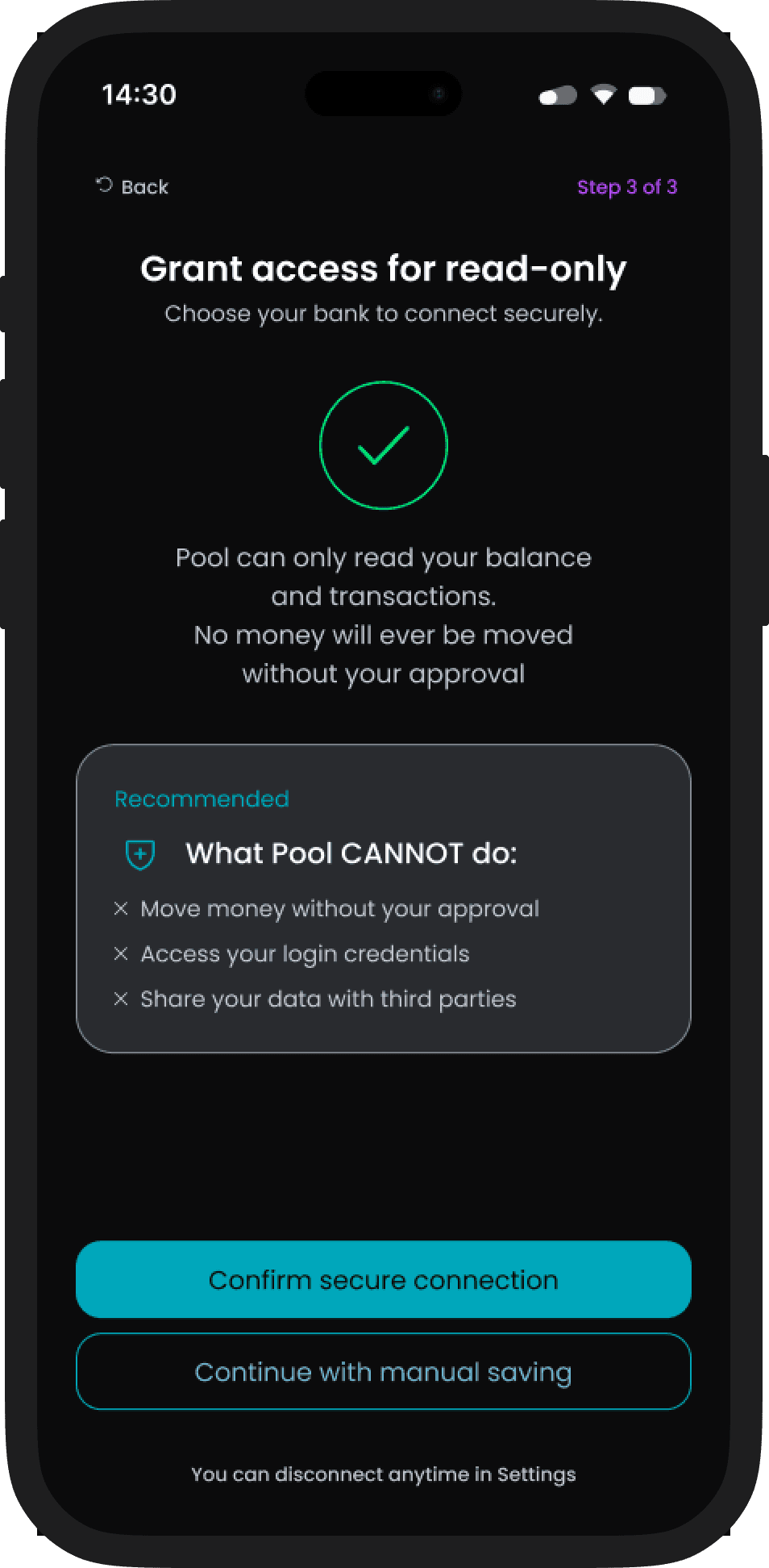

Contribution Flow

What this enables: flexible inputs that feed the same shared model, whether you log manually or sync a bank.

What this enables: flexible inputs that feed the same shared model, whether you log manually or sync a bank.

What this enables: flexible inputs that feed the same shared model, whether you log manually or sync a bank.

Flexible input

Read-only bank sync

Trust by design

Start manual, connect later, read-only bank sync is optional

Progress is calculated the same way regardless of input method

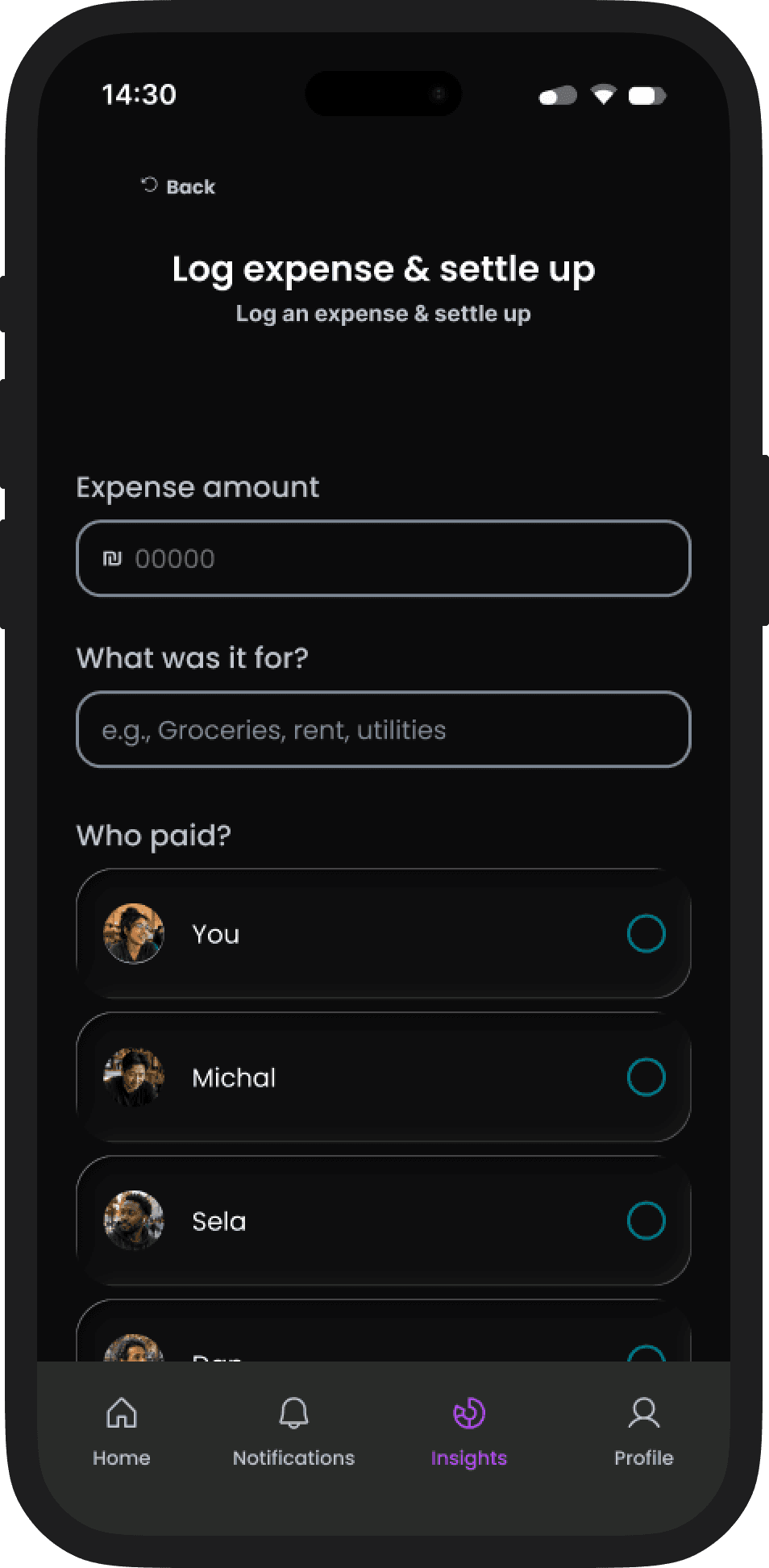

Log expense & settle up

Log expense & settle up

What this supports: logging shared costs and settling up without turning money into a social tension point.

What this supports: logging shared costs and settling up without turning money into a social tension point.

Expense logging

Settle up

No social friction

Quick logging with smart defaults for common shared costs

Quick logging with smart defaults for common shared costs

Clear settlements when it’s time to balance

Clear settlements when it’s time to balance

People don't download financial apps on impulse. They need to understand the model, trust the product with their bank, and feel confident it won't create friction in their group. The app can't answer those questions alone, so I designed a companion marketing site as part of the product experience, sharing the same tokens, voice, and color system.

People don't download financial apps on impulse. They need to understand the model, trust the product with their bank, and feel confident it won't create friction in their group. The app can't answer those questions alone, so I designed a companion marketing site as part of the product experience, sharing the same tokens, voice, and color system.

The App Needed a Front Door

The App Needed a Front Door

The Trust & Transparency page was designed to answer the question every potential user is silently asking before they hit download.

The Trust & Transparency page was designed to answer the question every potential user is silently asking before they hit download.

Outcome

Pool demonstrates that shared saving can work when the system removes the social friction. One mental model for solo and group goals, contribution status visible at a glance, and explicit read-only boundaries let people save together without asking where the money went.

Pool demonstrates that shared saving can work when the system removes the social friction. One mental model for solo and group goals, contribution status visible at a glance, and explicit read-only boundaries let people save together without asking where the money went.

What I'd measure

Goal Completion Rate

Did the group reach its savings target? This is the core promise of Pool. Low completion signals either unrealistic goals or contribution drop-off along the way.

Goal Completion Rate

Did the group reach its savings target? This is the core promise of Pool. Low completion signals either unrealistic goals or contribution drop-off along the way.

Active Participation Rate

How many group members contribute consistently over time? One active member in a group of four is a UX failure, not a user failure.

Active Participation Rate

How many group members contribute consistently over time? One active member in a group of four is a UX failure, not a user failure.

Bank Connect Completion

What share of users who start the bank sync flow complete it? Drop-off here signals a trust or clarity problem in the permissions screen.

Bank Connect Completion

What share of users who start the bank sync flow complete it? Drop-off here signals a trust or clarity problem in the permissions screen.

What This Proves

People don't save in fundamentally different ways alone or with others. They set a target, watch progress, adjust pace. Treating shared saving as a configuration of personal saving, rather than a separate product, cut cognitive overhead without closing the door on group dynamics. Every trust control and manual escape hatch serves one thesis: design that respects users' agency over their money.

People don't save in fundamentally different ways alone or with others. They set a target, watch progress, adjust pace. Treating shared saving as a configuration of personal saving, rather than a separate product, cut cognitive overhead without closing the door on group dynamics. Every trust control and manual escape hatch serves one thesis: design that respects users' agency over their money.

If the work made sense to you,

let's talk.

If the work made sense to you,

let's talk.

© 2026 Guy Bar-Sinai